Should you invest in an RRSP or TFSA?

Developing a retirement savings is critical for every successful entrepreneur. It’s never too early to start saving, so here is a guide to help you understand when it is better to invest in your Registered Retirement Savings Plan (RRSP) and when you should invest in your Tax Free Savings Account (TFSA.)

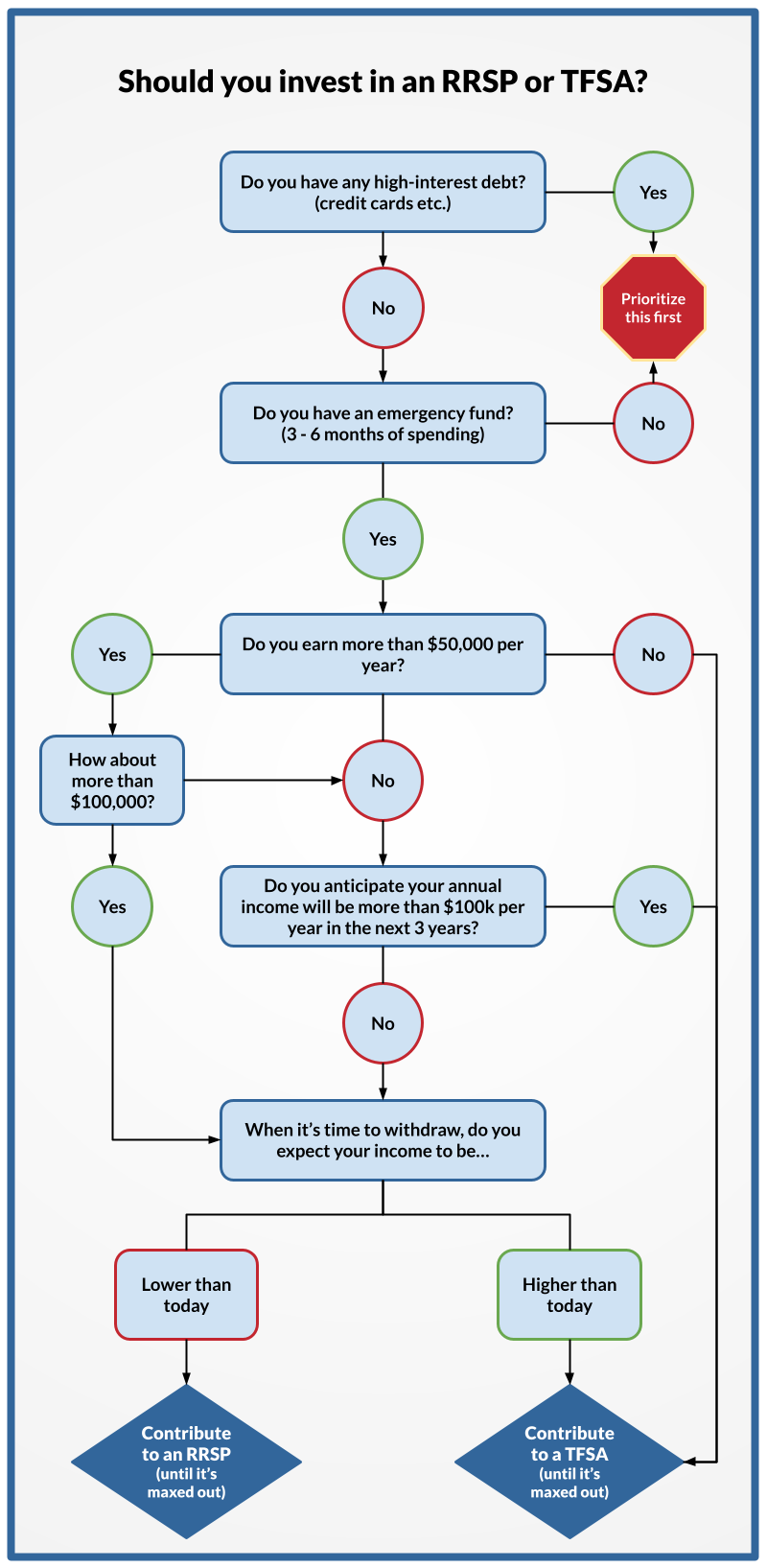

Both RRSPs and TFSAs shelter you from tax as long as the investments are held within the account and stay in the account. With an RRSP, you can deduct the contribution from your income, which earns you a tax refund at your highest marginal rate, but the money becomes fully taxable at your highest marginal rate when you take it out.

The TFSA is the reverse: you don’t get a tax break on contributions, but you don’t pay tax on withdrawals either. So if you’re deciding between the two options, it’s really a question of whether to pay the taxman now or later.

In general, if you believe you are in your highest earning years, you should favour RRSP contributions, and if you believe you are in a low-earning year, contributions to your TFSA are more favourable. If you expect your income to be higher in future years than it is in this current year, you’re usually better off saving your RRSP contribution room for your higher-earning years.

The RRSP deadline is approaching (February 29, 2024) so it’s time to take action.

Still unsure which investment works best for you?

Here’s a breakdown of contribution numbers for the RRSP:

*At 18% of income, max $30,780

**Refundable assuming all other income taxes paid (employment income for example)

Avoiding Over-Contributions

Over-contributing to your TFSA or RRSP can carry costly penalties, so it is important to monitor your contribution room when making deposits to these registered accounts.

TFSA and RRSP over-contributions are taxed at a penalty of 1% of the highest excess amount in the month, for each month that the excess amount stays in your account. With the RRSP, you have a cumulative lifetime over-contribution limit of $2,000 which acts as a buffer in case you accidentally exceed your limit temporarily. This buffer does not exist with the TFSA.

You can keep track of your contribution room each year by checking your Notice of Assessment (NOA) and logging in to CRA My Account online, and keeping your own running total of deposits made throughout the year.

What about the FHSA?

The First Home Savings Account (FHSA) is a relatively new registered account introduced by the federal government in 2022 that is designed to help you to save for your first home.

This account allows you to save and invest up to $8,000 per year (starting in the year you opened your account) towards your first home, and claim a tax deduction on qualifying contributions for the year of contribution, with a lifetime contribution limit of $40,000.

To withdraw your savings tax-free and make a “qualifying withdrawal”, you must be in the process of buying your first home, and meet all conditions listed by the CRA.

For more information, see our post on Understanding the First Home Savings Account (FHSA). You can also review CRA guidelines for the most up-to-date information on this account.

Disclaimer: This commentary is provided for general informational purposes only and does not constitute financial, investment, tax, legal or accounting advice nor does it constitute solicitation to buy or sell any securities referred to. Any tax information published on this blog is based on the facts provided to us and on current tax law (including judicial and administrative interpretation) during the time of publication. Tax law can change (at times on a retroactive basis) and these changes may result in additional taxes, interest, or penalties. Practice due diligence and if in doubt, speak with a member of our team.